Global Fundraising Outlook

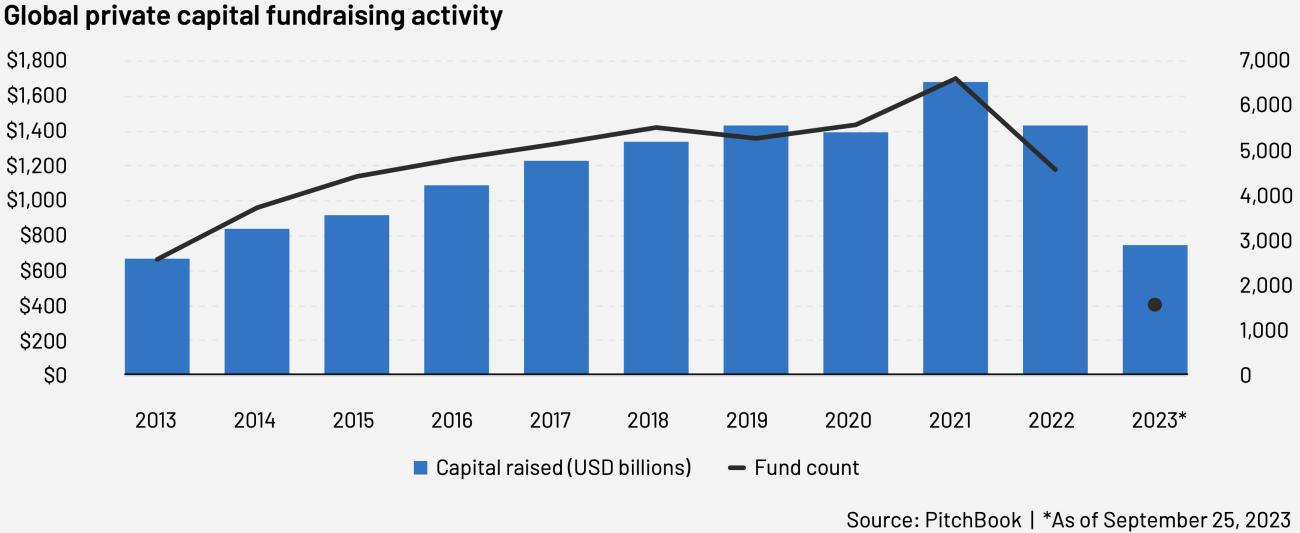

According to SS&C’s Intralinks Global Fundraising Outlook, private capital fundraising has reached USD 735.9 billion across 1,563 funds in the year to date (YTD), representing just over half the amount raised in 2022 and signaling a continued moderate slowdown from the record high reached in 2021. 2022 introduced a broader market downturn, and private funds felt this in the form of slower fundraising.Yet funds were still able to attract significant amounts of capital — in fact, 2022 marked the third-highest year on record for total capital raised.

The number of funds that drove this amount, however, reveals another story. There was a noticeable 30.8 percent drop in the number of funds actively raising between 2021 and 2022, and this population continues to dwindle in 2023. YTD fund count represents about one-third of 2022's count, while YTD capital raised represents more than half of 2022's. In other words, the population of funds that are actively raising capital is declining faster than the cumulative amount of capital they are raising. Fewer private funds have been able to attract new commitments as LPs contend with the denominator effect and increasingly prefer experienced managers. Selectivity has grown across the board as general partners likewise raise the bar for new portfolio additions in a slower dealmaking arena for most strategies.

Even among the smaller population of funds successfully closing in this tighter environment, funds are taking slightly longer to complete the process, with a median time to close of 14.4 months YTD compared with the median of 12 months in 2022. Portfolio reassessments and operating plans may take precedence over raising additional funds for new investments. In the U.S., new rules for private funds were recently adopted by the Securities and Exchange Commission (SEC) with the intention of increasing transparency for LPs. These new rules may create longer administrative timelines for closing funds in the coming quarters as firms update compliance practices.

Concentration of capital among established funds with greater perceived protection against headwinds has resulted in larger — and in many cases record-high — fund sizes this year. Median fund sizes have grown for most strategies except for Real Estate, which saw its median fund size drop 14 percent YTD. Private equity (PE) and secondaries funds saw the greatest increases in their median fund sizes over the same period, with 158 percent and 257 percent growth, respectively.

The smallest funds are feeling the low-liquidity environment most acutely, as evidenced by a reduced proportion of total fund count attributed to funds under USD 50 million. Just 554 such funds have raised capital YTD, compared with 1,848 in 2022. Tangentially, first-time fundraising activity unsurprisingly dropped as investors flocked to the most trusted and experienced managers. However, total capital raised for first-time funds so far in 2023 still represents more than half the amount raised last year, indicating that barriers entry for first-time funds are high but not insurmountable. In the SS&C Intralinks 2024 LP Survey, respondents that planned to allocate to emerging managers cited attractive return on potential niche strategy options (50 percent), added portfolio diversification (30 percent), and desire to access new talent (17 percent) as their main drivers.